|

|

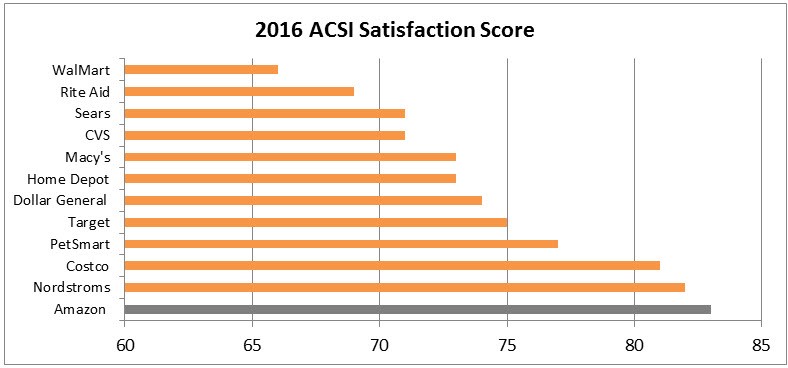

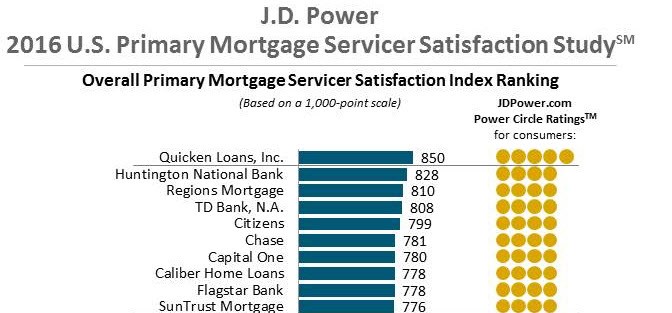

Consumer Lending Disruptors - Friend or FoeMany banks are now buying loans originated by online lenders such as Lending Club, Prosper and OnDeck. The underlying question is, how effective is each originator's credit model? Credit models have not been proven out over time, but their effectiveness is key to success. A secondary question is, does the purchasing bank have better use for their capital? For some banks, purchasing loans from these lenders is absolutely the right move as it leverages capital, increases diversification and puts underperforming equity to work. However, just like any other business, dabbling doesn’t work here either. Partnering with online lenders can be a valuable learning experience. Still, for some banks, purchasing these assets are a strategically bad move as they can gain better risk-adjusted returns elsewhere and their investment in these loans from online lenders represents a negative credit arbitrage for the bank as these assets are underpriced given the risk. Regardless of which camp you fall into, every banker should consider what the future of online lending holds and how to best position themselves for the coming disruption. The Competitive Advantage of Online Lenders Each year that passes, more and more lending segments are moving toward a complete online experience. Today we have consumer, mortgage, SBA, franchise loans and other segments fully automated. Many banks take comfort in the fact that larger loans and commercial real estate are too complicated to be automated and do not see online offerings as a threat in those segments. I wouldn’t be as sanguine about this issue. We have recently seen commercial real estate loans offered completely online for the first time in history. This is toothpaste that cannot be put back in the tube. The economics are too compelling. Instead of originating loans at, say, a 75% efficiency ratio, these online platforms originate loans at a 15% efficiency ratio. While currently less than 10% of CRE loans are originated online, this disparity in economics will become more of a factor going forward. Some predict that in three short years, online lending will comprise over 50% of loan production. What will traditional banks do then, facing a major origination and servicing cost disadvantage relative to their online brethren? Further, many online lenders are also employing data, analytics and machine-learning to both marketing as well as credit, which means that their cost of acquisition and capital allocation are also a fraction of the traditional bank’s costs. Online lenders will have a fraction of the overall cost and capital compared to banks when these elements are combined. If online lenders can operate at better margins and/or originate at lower fees and lower interest costs, traditional banks will have to paddle much faster to achieve the same results without losing market share. Some say this is a lost cause, because the convenience offered online is unparalleled. In short: Soon, online lending will be cheaper, faster and more accurate. Traditional banks’ response - Service Will Protect Us The most frequent response I get when I bring up online competition is – “our bank is protected because of our superior service”. I recall bankers said the same thing about mortgages until Quicken took the top spot in customer satisfaction last year. Similarly, how many traditional retailers have higher satisfaction than Amazon? The startling answer is depicted below.

All is not lost These charts do not mean that traditional banks don’t have an advantage. Our cost of capital, leverage capabilities, funding sources and cost as well as (some question this) our position of high public trust are serious strategic advantages. The combination of all these factors primarily leads to one conclusion – both business models are meritorious, and a combination of both is invaluable. Some online lenders have and will be acquired by banks, and some will acquire a bank. Ultimately banks will either have to develop a competing platform or partner with available platforms to originate their own loans for a license fee. This is likely inevitable and in any case likely a positive addition for most banks in this country. This issue needs to be in every community bank’s strategic plan and board agenda. If Bank A has an online platform and Bank B does not, and all other things being equal, the more efficient business model of Bank A can pay a higher price for Bank B as Bank A will recognize more cost savings through additional automation using fintech-acquired technology. Facing the future

We are quickly approaching the déjà vu moment of realizing how valuable deposits are. The war for deposits hasn’t erupted yet, and many of us rest easy with the knowledge that we have excellent and stable funding sources.

In general, deposits are not too complicated in terms of customer acquisition and retention attributes as well as product features and servicing. Further, most households prefer their deposits local for ease of access. As a result, many Internet-only banks could initially attract customers only through high-rate product offerings. Many deposit-only online banks haven’t demonstrated a clear “win”. This is not the case for online lending.

Online lending, if done right, is a clear win. As these online lenders expand market share, banks will discover that, like mortgages, borrowers are less geographically tied to local institutions and are more likely to take personal capital from online providers. The net result is that online lenders are likely to have an even greater impact than internet-only deposit-focused banks on the traditional community bank’s future.

Strategizing

This is a unique time in our industry’s evolution. As we travel through these uncharted waters, it is advisable for each bank to outline basic tenants to guide you in your strategic pathing. Think through fundamental questions such as:

• How important or practical is self-reliance?

• Does technology delivery threaten your culture and/or your ability to deliver on your brand promise?

• Who owns the customer in partnership arrangements and how can you assure retention of that customer ownership?

• How important is your brand?

• How can you express your brand through technology?

• Who controls, manages and secures your data?

• What technology and services will be “table stakes” in 3 and 5 years?

• Ultimately, where does you bank add value to customers?

I have written in the recent past about Fintech disruptors and generally my feeling is this – if you can’t beat them, join them. This article is aimed at moving you toward taking the next step; namely, figuring out how can you address this revolution profitably, effectively and with positive customer impact.

|